Examples

Feature Selection (Step-by-Step)

Start by ranking all features by Information Value:

from sklearn.datasets import fetch_openml

from sklearn.model_selection import train_test_split

from ScoreCardModel.analytics.selection import rank_features

COLUMN_MAP = {

'x1': 'LIMIT_BAL', 'x2': 'SEX', 'x3': 'EDUCATION', 'x4': 'MARRIAGE', 'x5': 'AGE',

'x6': 'PAY_0', 'x7': 'PAY_2', 'x8': 'PAY_3', 'x9': 'PAY_4', 'x10': 'PAY_5', 'x11': 'PAY_6',

'x12': 'BILL_AMT1', 'x13': 'BILL_AMT2', 'x14': 'BILL_AMT3', 'x15': 'BILL_AMT4',

'x16': 'BILL_AMT5', 'x17': 'BILL_AMT6',

'x18': 'PAY_AMT1', 'x19': 'PAY_AMT2', 'x20': 'PAY_AMT3', 'x21': 'PAY_AMT4',

'x22': 'PAY_AMT5', 'x23': 'PAY_AMT6',

}

data = fetch_openml('default-of-credit-card-clients', as_frame=True,

parser='pandas', version=1)

X = data.data.rename(columns=COLUMN_MAP)

y = (data.target == '0').astype(int)

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.3, random_state=42

)

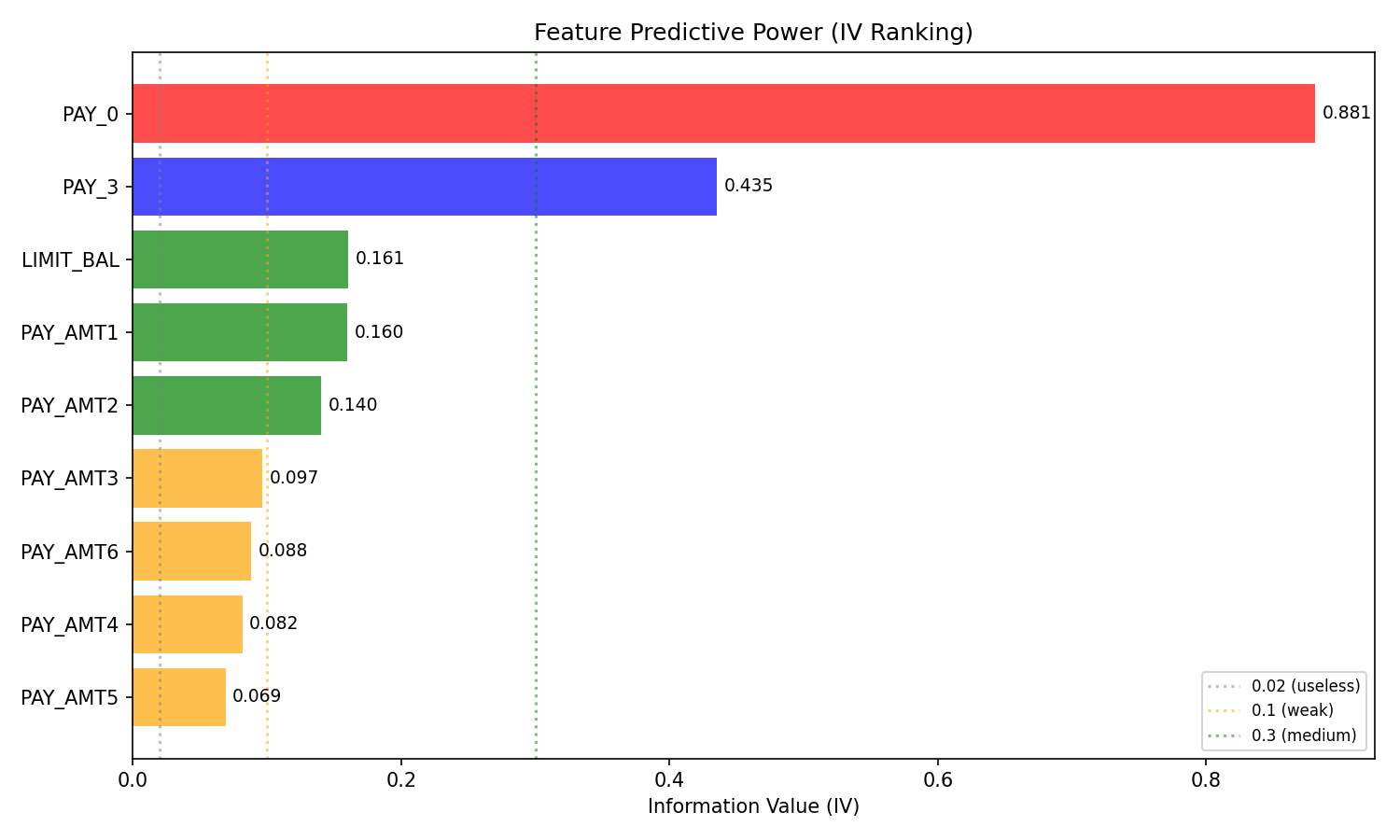

ranking = rank_features(X_train, y_train, n_bins=5)

print(ranking)

Output (23 features ranked by IV):

Feature IV IV_Label Monotonicity ... Chi2_pvalue Recommendation

0 PAY_0 0.8816 suspicious decreasing ... 0.0000 Investigate

1 PAY_2 0.5704 suspicious decreasing ... 0.0000 Investigate

2 PAY_3 0.4354 strong non-monotonic ... 0.0000 Accept

3 PAY_4 0.3673 strong non-monotonic ... 0.0000 Accept

...

12 PAY_AMT5 0.0694 weak increasing ... 0.0000 Accept

13 EDUCATION 0.0193 useless non-monotonic ... 0.0000 Reject

...

21 MARRIAGE 0.0057 useless non-monotonic ... 0.5000 Reject

22 SEX 0.0000 useless single_bin ... 1.0000 Reject

Feature names are mapped from the original UCI dataset (PAY_0–PAY_6 = repayment status history, LIMIT_BAL = credit limit, PAY_AMT1–PAY_AMT6 = payment amounts, etc.).

The Recommendation column guides the decision:

- Reject — IV < 0.02 (useless)

- Accept — IV 0.02–0.5 (weak to strong)

- Investigate — IV > 0.5 (suspicious — review manually)

Filter to "Accept" features, then add "Investigate" ones that are monotonically decreasing (ideal for scorecards). Finally, remove highly correlated features:

from ScoreCardModel.analytics.selection import select_by_correlation

accept = ranking[ranking['Recommendation'] == 'Accept']['Feature'].tolist()

investigate = ranking[

(ranking['Recommendation'] == 'Investigate') &

(ranking['Monotonicity'] == 'decreasing')

]['Feature'].tolist()

candidates = accept + investigate

print(f'Candidates: {len(candidates)} features')

final = select_by_correlation(X_train[candidates], max_corr=0.7)

print(f'After correlation filter: {len(final)} features')

print(final)

Output:

Candidates: 13 features

After correlation filter: 9 features

['PAY_3', 'LIMIT_BAL', 'PAY_AMT1', 'PAY_AMT2', 'PAY_AMT3', 'PAY_AMT6', 'PAY_AMT4', 'PAY_AMT5', 'PAY_0']

End-to-End Pipeline

from sklearn.pipeline import Pipeline

from sklearn.linear_model import LogisticRegression

from ScoreCardModel import BinningTransformer, WOETransformer

from ScoreCardModel.analytics.metrics import calculate_ks

pipeline = Pipeline([

('binning', BinningTransformer(n_bins=5)),

('woe', WOETransformer(method='empirical_logit')),

('model', LogisticRegression(max_iter=1000)),

])

pipeline.fit(X_train[final], y_train)

y_prob = pipeline.predict_proba(X_test[final])[:, 1]

ks = calculate_ks(y_test, y_prob)

print(f'KS: {ks:.3f}')

Output:

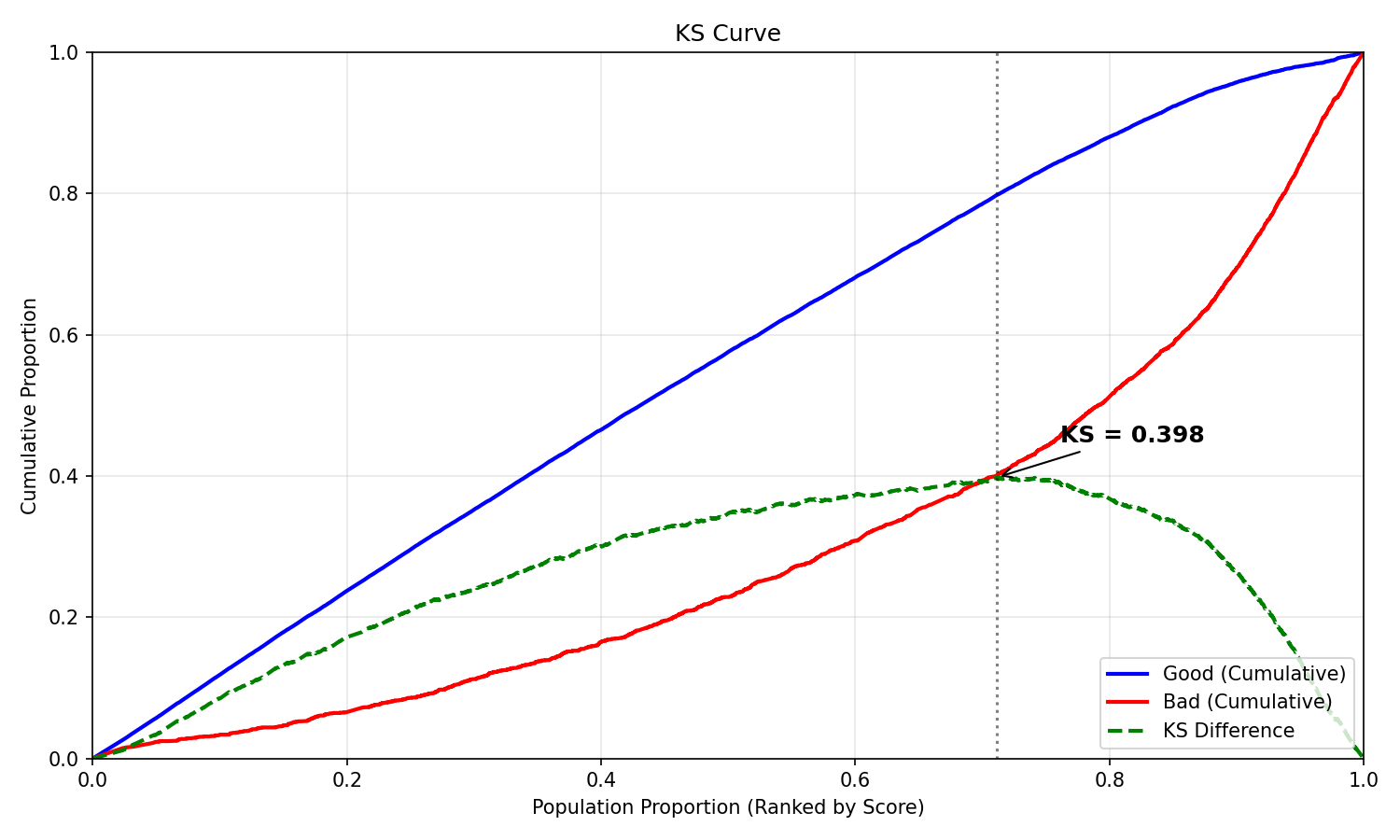

KS: 0.398

Export scorecard table:

from ScoreCardModel.score_card.transformers import ScoreCardTransformer

lr = pipeline.named_steps['model']

bt = pipeline.named_steps['binning']

wt = pipeline.named_steps['woe']

sct = ScoreCardTransformer(lr, bt, wt)

card = sct.export_scorecard()

print(card.head(10))

Output:

Variable Bin WOE Points

PAY_3 (-1.0, 0.0] 0.304362 62.04

PAY_3 (-inf, -1.0] 0.353610 62.67

PAY_3 (0.0, inf] -1.393825 40.22

LIMIT_BAL (-inf, 50000.0] -0.520152 51.85

LIMIT_BAL (100000.0, 180000.0] 0.159326 60.05

LIMIT_BAL (180000.0, 270000.0] 0.301749 61.77

LIMIT_BAL (270000.0, inf] 0.589377 65.24

LIMIT_BAL (50000.0, 100000.0] -0.165176 56.13

PAY_AMT1 (-inf, 316.0] -0.638325 52.43

PAY_AMT1 (1714.0, 3000.0] 0.042485 58.50

Visualizations

All plots are generated from a model trained on the Taiwan Credit dataset with 9 features selected via rank_features() + select_by_correlation(). The plots below are real output — not mockups.

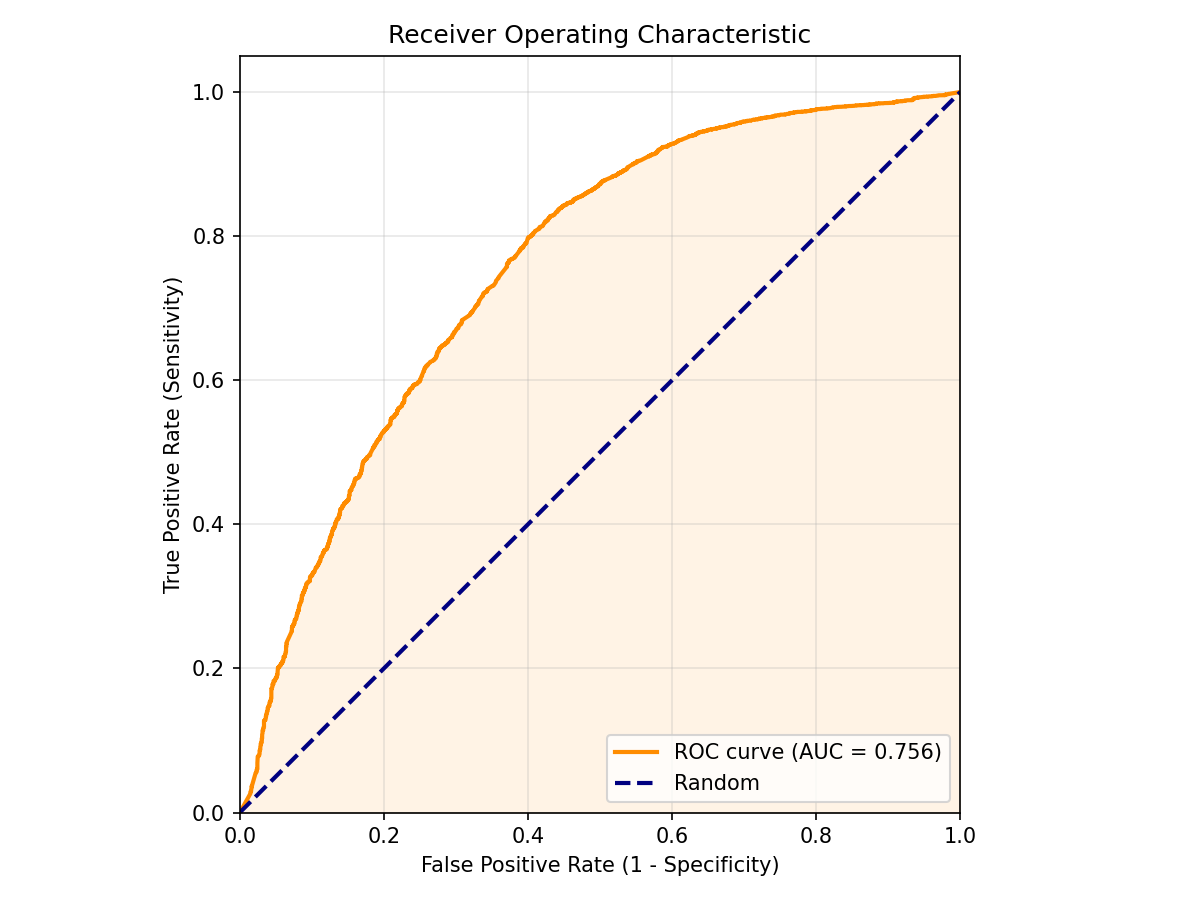

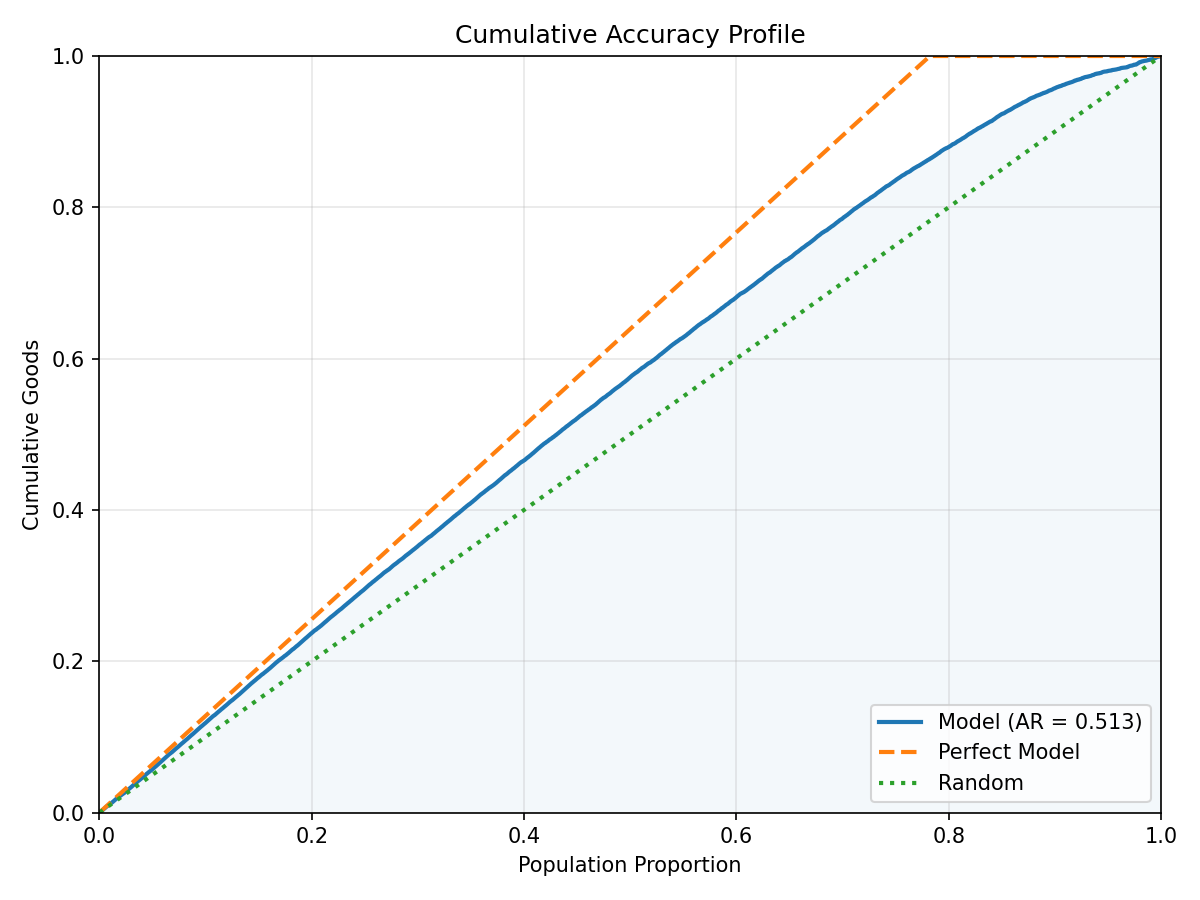

Model Discrimination

| KS Curve | ROC Curve | CAP Curve |

|---|---|---|

|

|

|

KS measures the maximum separation between good and bad populations. ROC shows the trade-off between TPR and FPR. CAP (Cumulative Accuracy Profile) shows the model's cumulative lift over random selection.

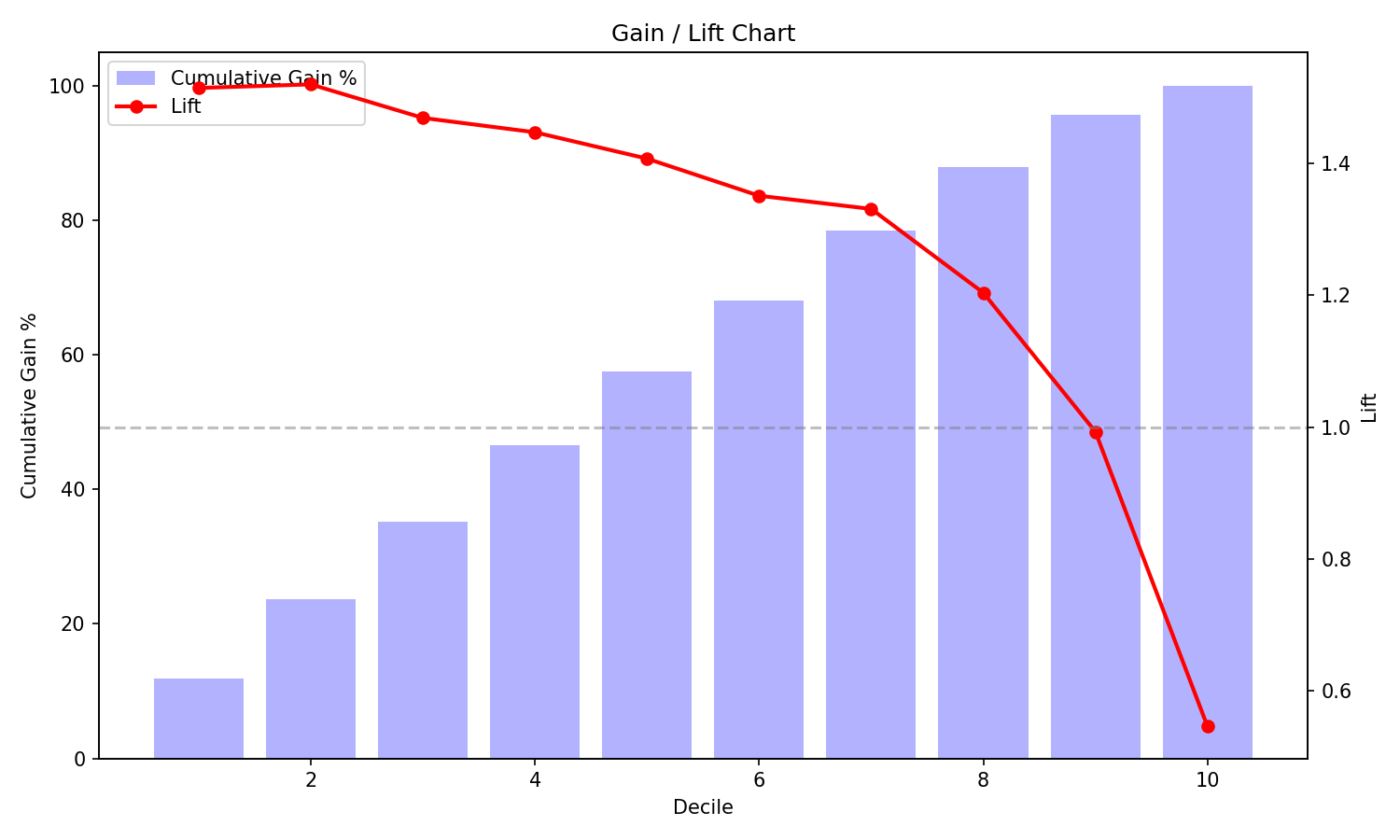

Performance Diagnostics

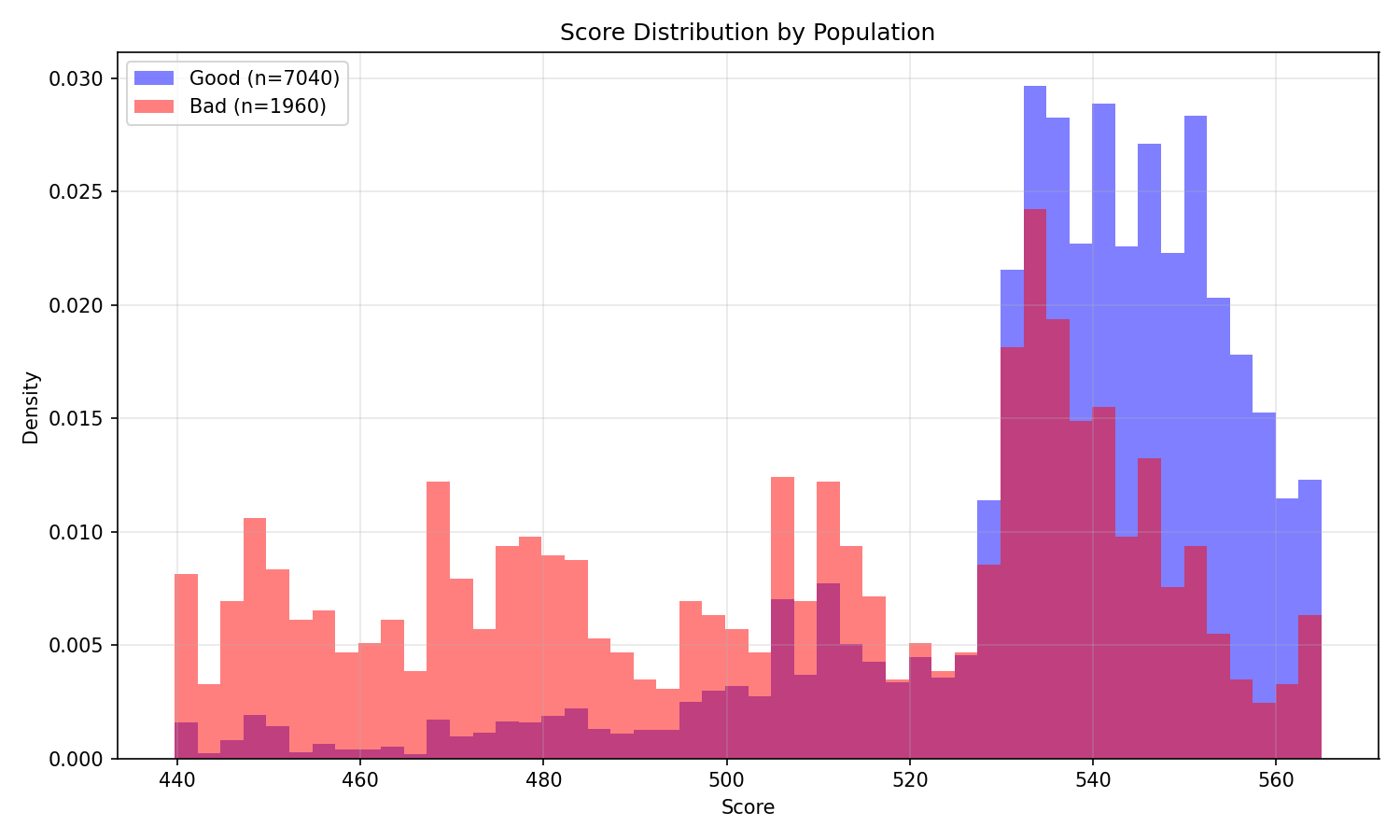

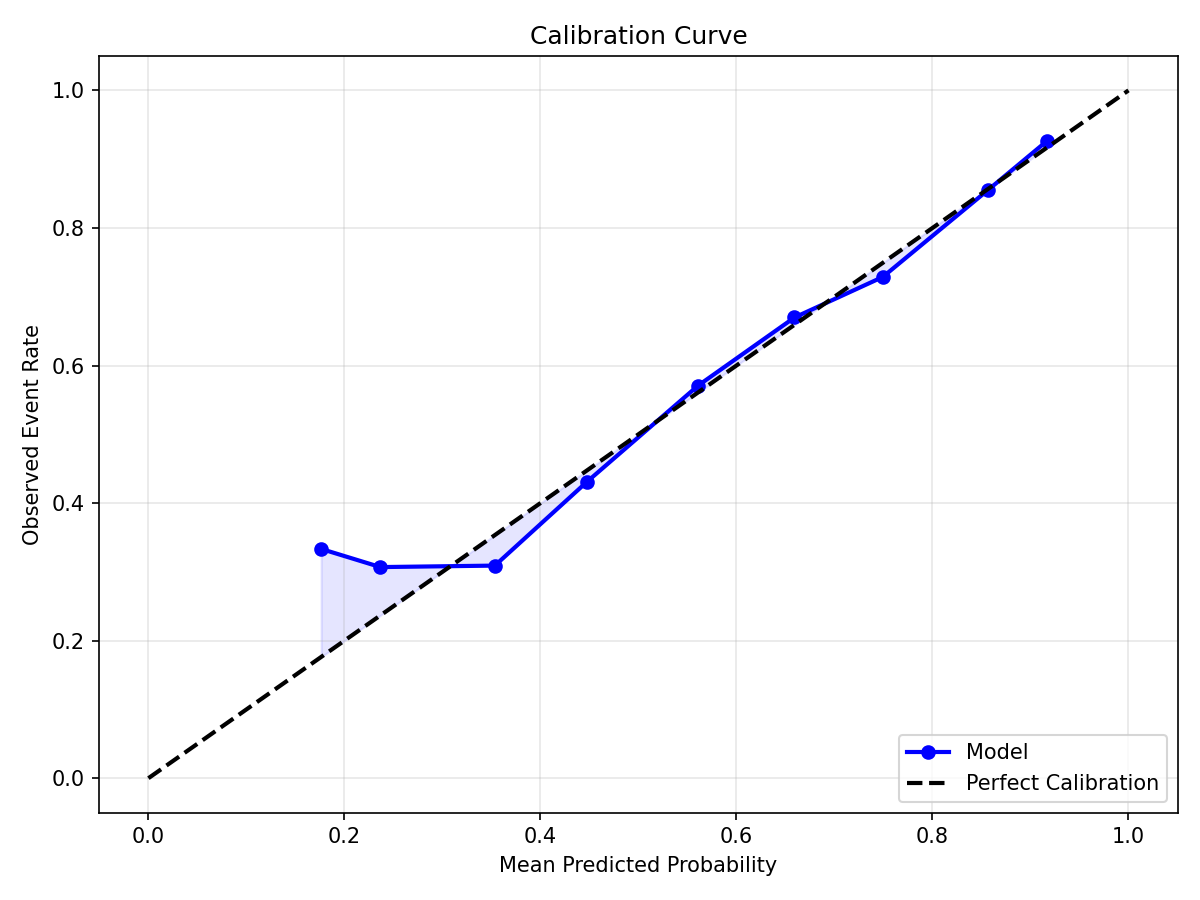

| Gain / Lift | Score Distribution | Calibration |

|---|---|---|

|

|

|

Gain/Lift charts show how well the model ranks risk at each decile. Score distribution compares score profiles of good vs bad accounts. Calibration plots assess whether predicted probabilities match observed event rates.

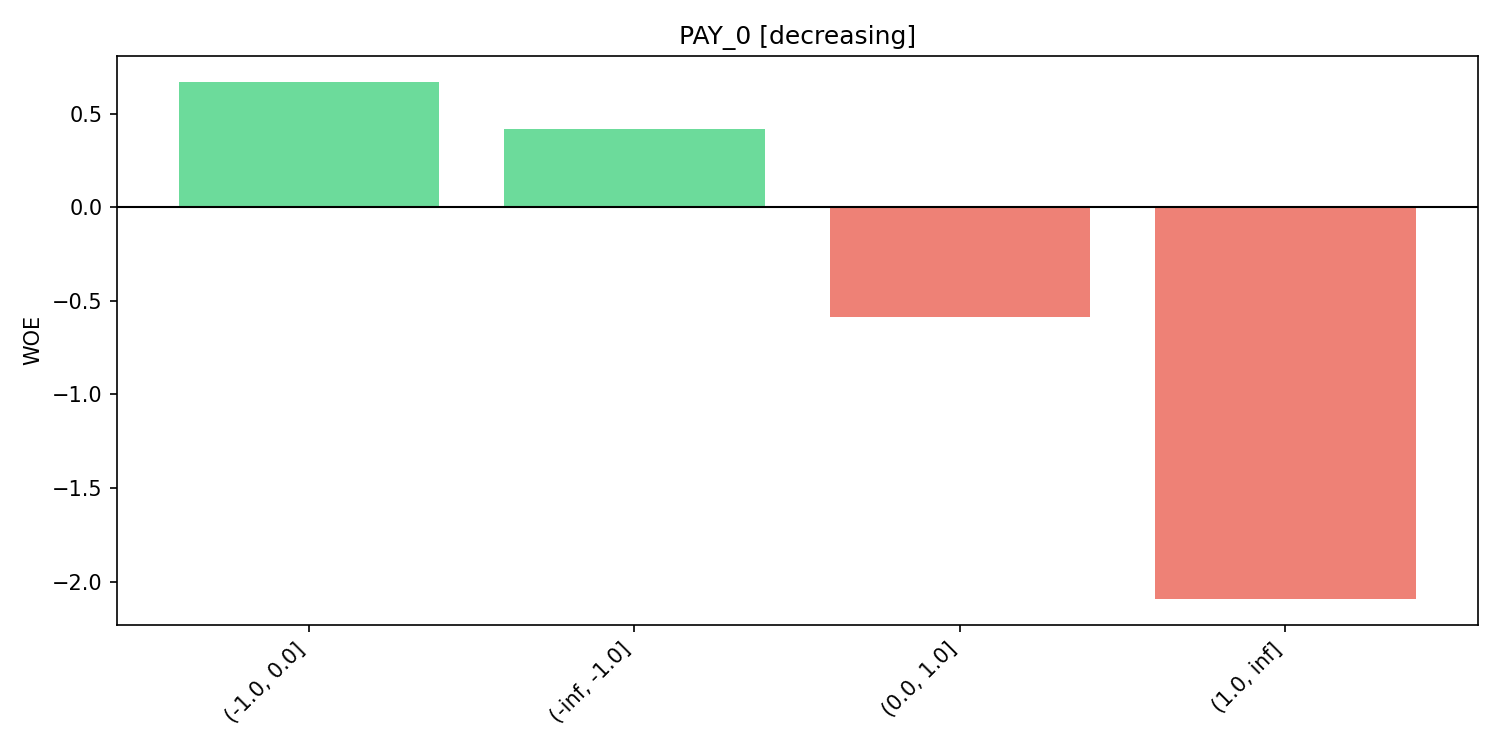

WOE and IV Analysis

| WOE Pattern | IV Summary |

|---|---|

|

|

WOE pattern plots show the relationship between bins and their Weight of Evidence. IV summary ranks features by Information Value for feature selection.

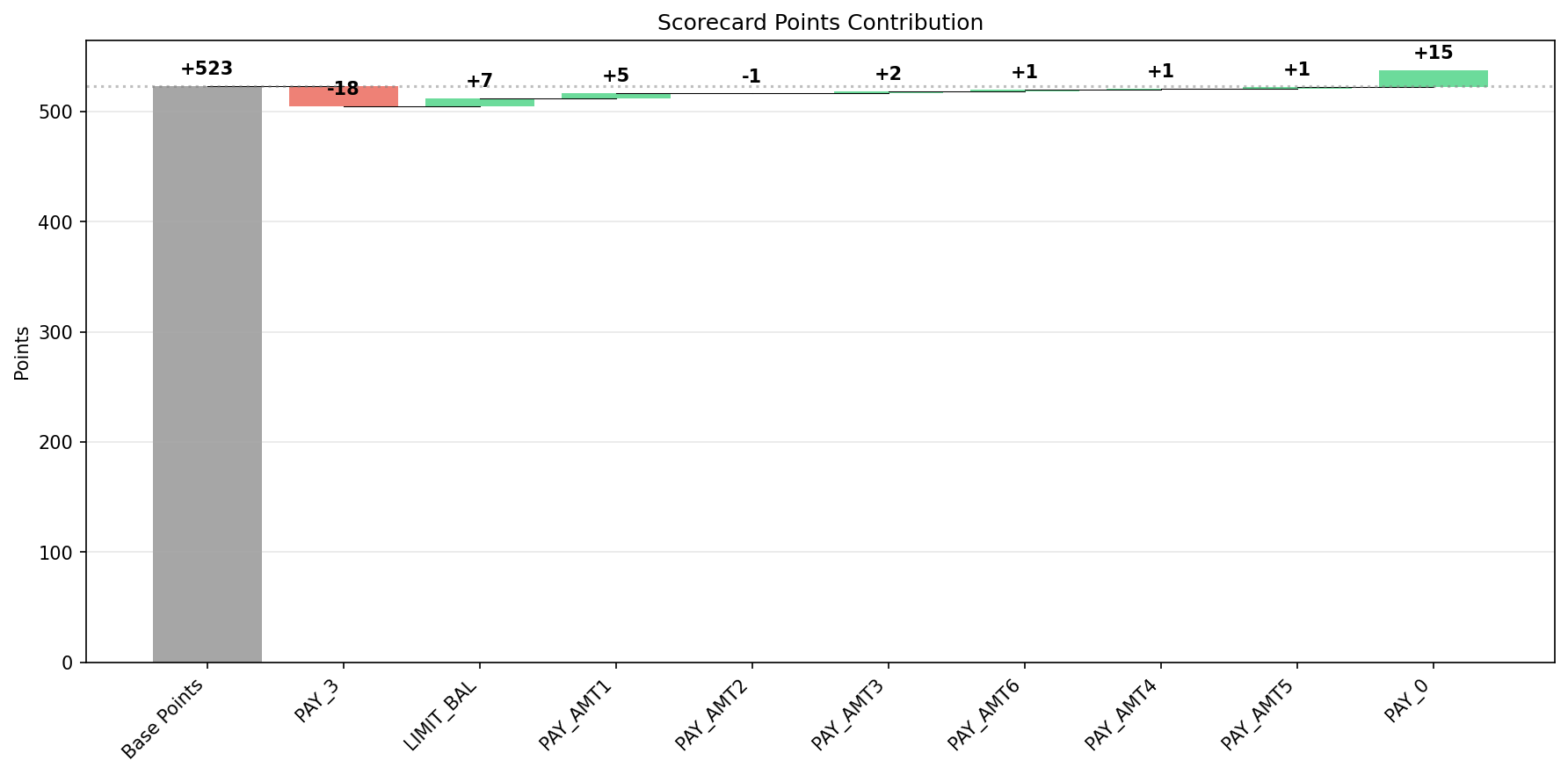

Scorecard Interpretation

| Scorecard Waterfall | Scorecard Heatmap |

|---|---|

|

|

Waterfall charts show how each feature contributes to the final score. Heatmaps provide a bird's-eye view of the scorecard table.

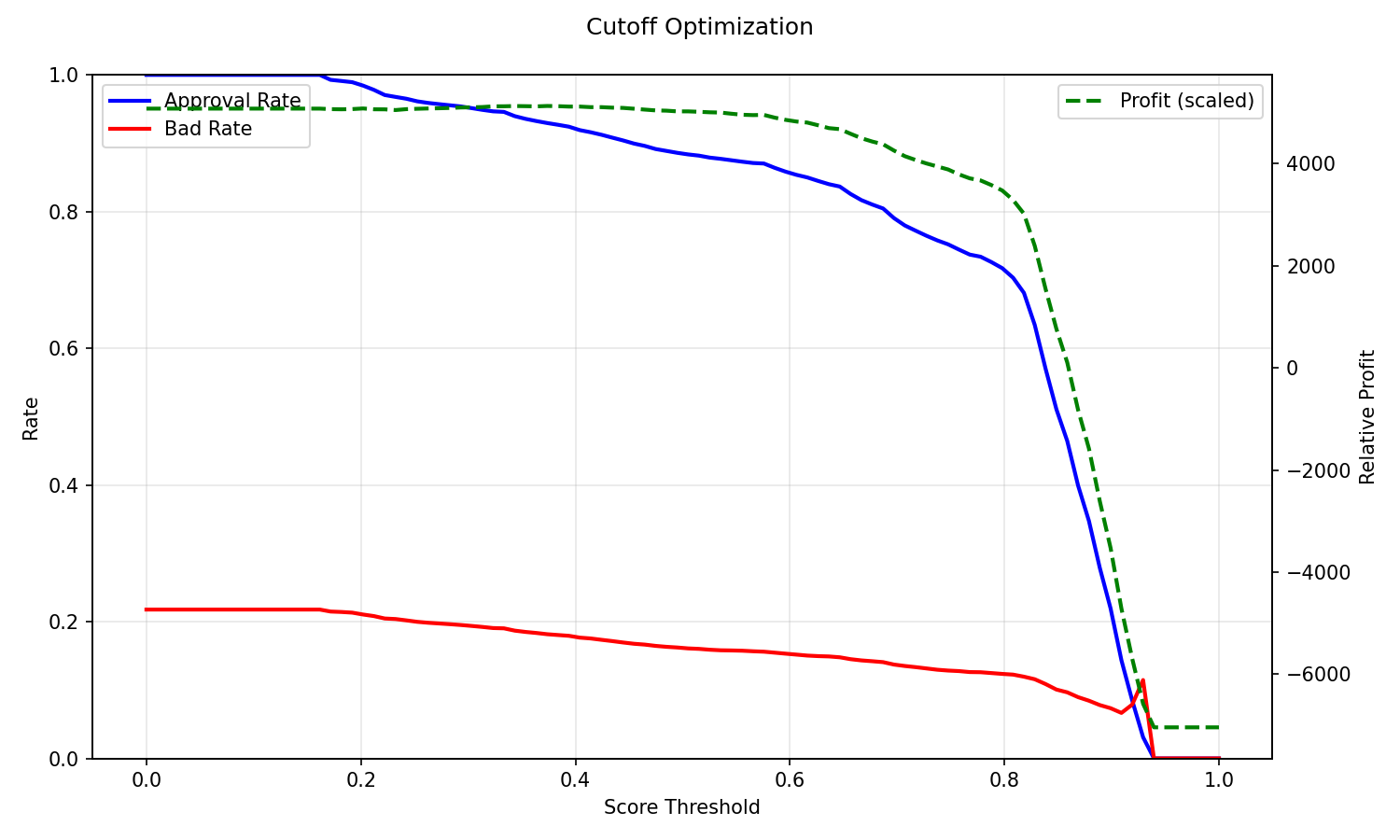

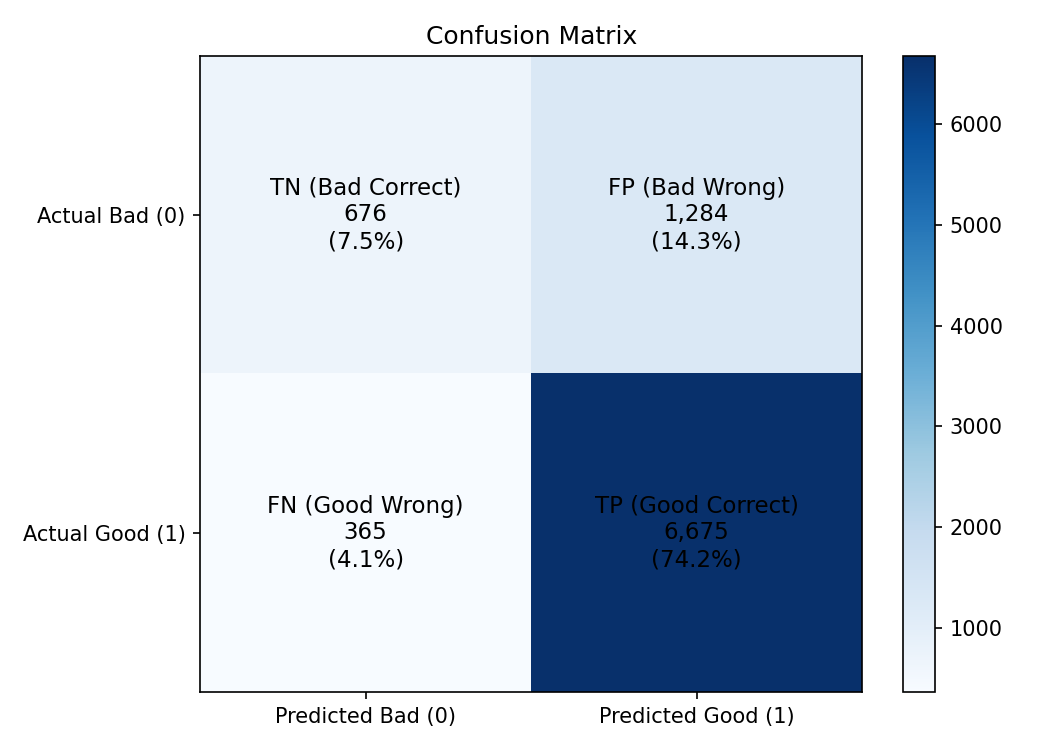

Decision Threshold

| Cutoff Optimization | Confusion Matrix |

|---|---|

|

|

Cutoff optimization identifies the optimal decision threshold by balancing cost/benefit. The confusion matrix shows classification performance at the chosen cutoff.

Automated Report

from ScoreCardModel.analytics.reporting import generate_report

generate_report(pipeline, X_train, y_train, X_test, y_test,

output_path="scorecard_report.md")

The report is a markdown file with embedded PNG plots and the full scorecard table — suitable for sharing with stakeholders or regulatory review.

Interactive What-If Widget (Jupyter)

# Requires: pip install scorecard-toolkit[interactive]

from ScoreCardModel.interactive import ScorecardWidget

widget = ScorecardWidget(pipeline, X_train)

widget.display()

Opens an interactive dashboard in the notebook: sliders/dropdowns for each feature, real-time score display, and a live waterfall chart. The widget is purely client-side — no server needed.

Dataset Examples

The following examples demonstrate the full scorecard workflow on four real-world datasets spanning different domains, sizes, and data types.

German Credit

- 1,000 rows, 20 features (7 numeric + 13 categorical)

- 30% default rate

- Demonstrates mixed-type handling — categorical features are auto-detected by

BinningTransformer - Full report includes score distribution, KS curve, ROC, scorecard table, and cutoff analysis

data = fetch_openml('credit-g', as_frame=True, parser='pandas')

X, y = data.data, (data.target == 'good').astype(int)

ranking = rank_features(X_train, y_train, n_bins=4)

final = ranking[ranking['Recommendation'].isin(['Accept', 'Investigate'])]['Feature'].tolist()

# 13 features selected

KS: 0.481

Taiwan Credit (Default of Credit Card Clients)

- 30,000 rows, 23 numeric features

- 22% default rate

- Features renamed from x1–x23 to UCI names (PAY_0–PAY_6 = payment status, LIMIT_BAL = credit limit, PAY_AMT1–PAY_AMT6 = payment amounts, etc.)

- Demonstrates large-dataset performance with 9 selected features (after correlation filter)

data = fetch_openml('default-of-credit-card-clients', as_frame=True, parser='pandas', version=1)

X = data.data.rename(columns=COLUMN_MAP)

y = (data.target == '0').astype(int)

ranking = rank_features(X_train, y_train, n_bins=5)

final = select_by_correlation(X_train[candidates], max_corr=0.7)

# 9 features: PAY_0, PAY_3, LIMIT_BAL, PAY_AMT1–PAY_AMT6

KS: 0.398

Give Me Some Credit

- 150,000 rows, 10 features (6 integer + 4 float)

- 6.7% default rate — heavily imbalanced

- Requires missing value imputation for

MonthlyIncome(20% NaN) andNumberOfDependents(2.6% NaN) - Demonstrates imbalanced dataset handling with 6 selected features

data = fetch_openml('give-me-some-credit', as_frame=True, parser='pandas', version=1)

X, y = data.data, (data.target == '0').astype(int)

X['MonthlyIncome'] = X['MonthlyIncome'].fillna(X['MonthlyIncome'].median())

X['NumberOfDependents'] = X['NumberOfDependents'].fillna(0)

ranking = rank_features(X_train, y_train, n_bins=10)

final = accept + investigate # 6 features

KS: 0.368

WOE Method Comparison

The library provides 5 WOE methods. Each transforms bin counts into Weight of Evidence differently. The table below compares their performance on the Breast Cancer dataset:

## WOE Method Comparison (5 bins)

| Method | KS | AUC | Total IV |

|:----------------|-------:|-------:|-----------:|

| standard | 0.9841 | 0.9975 | 52.5544 |

| adjusted | 0.9683 | 0.9974 | 115.201 |

| empirical_logit | 0.9841 | 0.999 | 67.7484 |

| signed | 0.9841 | 0.9975 | 52.5544 |

| weighted | 0.9497 | 0.9979 | 10.5295 |

Key observations: - standard — raw ln(dist_good/dist_bad). Highest discriminatory power but can produce ±inf for zero-count bins (handled internally by replacing with 0). - adjusted — default method. Laplace smoothing (1e-6) prevents log(0) with negligible bias. Recommended for most use cases. - empirical_logit — Agresti correction (+0.5). Standard in SAS-based scorecard development. Robust for small bin counts. - signed — symmetric around zero using ln(max/min). Useful when direction matters more than magnitude. - weighted — downweights small bins by population share. Produces lower total IV but can be more stable with uneven bin sizes.

All 5 methods converge on similar KS/AUC when bins are well-populated. Differences emerge with sparse data, extreme class imbalance, or very small bin counts.

# Try different WOE methods

for method in ['standard', 'adjusted', 'empirical_logit', 'signed', 'weighted']:

pipeline = Pipeline([

('binning', BinningTransformer(n_bins=5)),

('woe', WOETransformer(method=method)),

('model', LogisticRegression(C=1.0)),

])

pipeline.fit(X_train, y_train)

y_prob = pipeline.predict_proba(X_test)[:, 1]

print(f"{method:16s} KS={calculate_ks(y_test, y_prob):.4f}")